BLOG -

Germany’s tighter FDI regime and the EU‘s path to uniform standards

1. The general investment environment in Germany

Foreign Direct Investment (FDI) in Germany has recently gained even greater significance than it has already gained over the past few years and Germany continues to attract large inflows of funds from EU and non-EU countries. FDI flows to and from Germany have increased in recent years. The largest German trading partners are at the same time among the biggest contributors to capital inflows, mainly through acquisitions and mergers. In the recent past, Chinese companies have increased their share of FDI and at one point Germany became the largest recipient, accounting for 31 percent of the total Chinese investment in the EU.1

Germany‘s great appeal as a favoured destination for investments is helped by its, by international comparison, rather “light” legal framework for company acquisitions and the fact that investments issued by third-country investors are only exceptionally subject to review, respectively to (i) a so-called sector-specific investment review and (ii) a general investment review.2

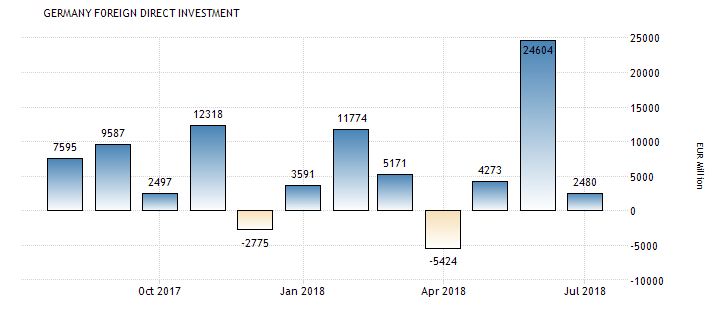

The graph illustrates the FDI rates for the past four quarters.

Source: https://tradingeconomics.com/germany/foreign-direct-investment

Yet, concerns have arisen about the possible loss of essential know-how and, in particular, key technologies to non-European investors, which would harm the competitive position on the markets concerned in the long run. These concerns became manifest in the acquisitions of German robotics manufacturer Kuka by the Chinese company Midea, of Aixtron SE by the Chinese investment fund Fujian Grand Chip, and the acquisition of LEDvance or a stake in Daimler by Geely. As a result, the quest is on for the establishment of a more effective regulatory framework but with the accompanying goal of not impeding the overall investment atmosphere.

2. The German legal conditions for investments

German authorities may subject investments by foreigners to (i) a so-called sector-specific investment review and (ii) a general investment review. The first concerns investments in the defence industry or IT security for classified information, whereas the second

review mechanism is of general nature and allows the acquisition to be reviewed where the investor is not a resident of the EU or European Free Trade Association (EFTA). In this context, the acquisition may only be prohibited if it substantially endangers German public order or security.

In spite of this liberal regulation, for legal certainty, we recommend that investors voluntarily notify their intended investment to the competent authorities when the target to be acquired is involved in activities that could even remotely give rise to public order or security concerns.

The German legal order also examines the competition on the market for the products concerned, according to the Act against Restraints of Competition (Gesetz gegen Wettbewerbsbeschränkungen - GWB). This review applies depending on the specific scale of the acquisition and is purely subject to legal criteria and market-economy based examination points, whilst disregarding political motives.

Of note are also sector-specific requirements, such as in the banking sector, though these equally do not allow political motives to be considered. A general tendency toward openness for investments can certainly be noted, for instance the BaFin, Germany’s Federal Financial Supervisory Authority, has expressly welcomed Chinese investment activity in the German banking sector in May 2017.

Cross-Sector Inquiries (Sektorübergreifende Prüfung von Unternehmenserwerben)

The Foreign Trade and Payments Ordinance (Außenwirtschaftsverordnung - AWV) lays down more precise rules on the circumstances under which the public order is potentially endangered and implements the level of security envisaged by the legislator; see Sections 55 - 59 AWV.3 In this case, the German Ministry for Economic Affairs and Energy (Ministry) is equipped with the po-wer to intervene, commence the review process and, where the assessment shows that it is appropriate, even entirely block takeovers. German public order or security concerns raised by an acquisition can be traced back to critical infrastructure, especially software in the fields of telecommunication, cloud computing, energy and water, finance and insurance, healthcare, transport and the food industry. Here, the Ministry must start its reviews three months after having received notice of the specific investment.

In order to obtain legal certainty before the expiry date (since the final deadline for opening an inquiry is currently set at five years after the conclusion of the acquisition agreement), the acquirer should propose a so-called certificate of non-objection.

Sector Inquiries (Sektorspezifische Prüfung von Unternehmenserwerb)

In the case of a sector inquiry, the target group concerned has been extended to include a wider range of defence and IT companies, see Sections 60 - 62 AWV. Companies producing or developing goods included in the export control list have now been added.

The latest Revisions to the Framework of the AWV

Starting with the 9th Regulation on the Amendment of the AWV of 14 July 2017 and continuing to the 11th and latest amendment of 5 January 2018, the German legislator has established a stricter set of rules for investments. These rules are designed to safeguard matters of public security, especially in relation to technological capacities in the arms sector and telematics infrastructure.

Based on a parliamentary act, amendment regulations for the AWV are adopted solely by the executive and at the present give the national Ministry the power to review acquisitions of a minimum of 25 percent investment share in national corporations by non-EU or – in case of misuse – EU corporations. As for the exact amendments, the 9th Regulation modified Article 55 et seq. on cross-sectoral review powers in the field of critical infrastructure and companies producing arms.

The 10th Regulation for the Amendment of the AWV of 28 September 2017 introduced a consolidated form of restrictive measures against investments to or from the Democratic People‘s Republic of Korea, as well as further amendments of the system of fines.

Lastly, the 11th Regulation on the Amendment of the AWV of 5 January 2018 implements the measures decided with respect to the arms embargo for Venezuela and the exemption regime for the EU-arms embargo for Russia into national law. In addition, this regulation contains more explicit rules on customs regulations and simplifying the procedure of investment control.

According to the revised rules, purchasers are obliged to register any acquisition in the industries mentioned in the Regulation with the Ministry. Furthermore, the Regulation foresees extended review periods, granting the Ministry a longer timeframe to review acquisitions i.e. appropriate measures must now be taken four months after notification in the case of cross-sector inquiries and within three months for sector inquiries. In this way, both, the sector-specific investment review on the one hand and the cross-sector investment review on the other, safeguard the maintenance of public security. The mechanisms only differentiate regarding to the respect that sector-specific inquiries contain stricter controls for more security-sensitive areas4.

The Latest Cases and Proposals

As mentioned above, Germany enacted stricter rules on foreign acquisitions of corporations in 2017 in response to increase interest from Chinese investors in buying companies with important technology and know-how. Now, on 1 August 2018, the stricter German rules on foreign investment were put to the test. Yantai, the leading company in nuclear casting and forging products, had planned to acquire German undertaking Leifeld, which was founded in 1891 and is a supplier of chipless metal forming, as well as the global technology leader for flow forming machines. It looked as if the acquisition of Leifeld Metal Spinning AG (Leifeld) by the Chinese Yantai Taihai Group (Yantai) would have been prohibited, had the acquirer not decided to withdraw its application on the day that the German Federal Government authorised the Ministry to prohibit the acquisition.

Though the Ministry is yet to release detailed grounds for the decision, it is likely that the envisaged prohibition was mainly based on concerns regarding the production of dual-use goods, which could be used in the defence sector, as well as in machines suitable for the production of nuclear-related goods.

In addition, the German Federal Government‘s actions to prevent a Chinese State-owned group from taking minority stake in 50Hertz, a German power grid operator, supports the conclusion that Germany is shifting towards a stricter review of acquisitions by State-owned groups and non-European investors. The current procedural structures and review mechanisms have been criticised as being highly ambiguous and lengthy, as well as for requiring burdensome undertakings from the parties concerned. This state of affairs does thus not only require patience but also a secured funding for the planned acquisition.

As regards 50Hertz, the Chinese State-owned company made two attempts to buy shares, both of which were thwarted. The first attempt failed when the Belgian network operator, Elia, increased its shareholding. On the second attempt, Elia again increased its shareholding, applying pre-emptive rights and bought the remaining minority shares from Australian Investment Fond IFM. This minority shareholding was then resold to the German national promotional Bank (Kreditanstalt für Wiederaufbau - KfW) with a future option to resell the shares.

The case of 50Hertz reveals important legislative gaps and supports the need to establish review powers for share acquisitions under 25 percent and possibilities to intervene in cases outside the scope of critical infrastructures. Current legislation proposals however push towards even tighter restrictions, and more specifically aim for a 10 - 15 percent threshold to provide for more comprehensive control powers.

At the same time, tougher measures are being applied against the backdrop of increased government-supported foreign direct investments in key national technologies where there is a strategic interest in transferring security-related technologies. Germany‘s primary goal is to take preventive measures against the transfer of accumulated know-how and sensitive data and to prevent any detrimental consequences to Germany‘s public security interests.5 Concerns about unwanted know-how transfers were sparked in particular by the secret acquisition of ten percent of Daimler by Chinese automotive conglomerate Geely. However, in this instance, Germany is faced with the constant struggle between safeguarding its unique selling point of innovative technologies and specialist know-how by blocking transactions and maintaining its pole position as preferred economic business partner. In light of the recent developments in the steel industry, triggered by the USA‘s actions, Germany is by mischance left “squeezed between two nationalistic superpowers”.6

The new direction of increased review efforts in Germany is also part of a global trend towards stricter investment control, with the Investment Risk Review Modernization Act (FIRRMA) on the US side, a National Security and Investment White Paper published by the UK Secretary of Business, and proposals at EU level (see under point 3.).

On this note, implementing a stricter regime should however not be confused with the ultimate goal of protectionism. In light of the vast number of successful Chinese investments in German companies in the past, which have enabled expansion without the harmful side effects of draining expertise and jobs7, genuine fears about the future of Germany‘s public security may be largely unfounded. However, the German Government, together with the Ministry, currently appears more keen on intervening in the case of foreign investments in areas essential for public security, i.e. to implement more intensive review transactions in connection with information technology, telecommunications, in the transport and traffic sector, health, water supply, food, as well as in finances and insurance.

The primary goal of the recently proposed amendments to the AWV is to regulate a lower review threshold of 15 percent, as opposed to the currently in place 25 percent mark, and to include security sensitive high technology branches within the material

scope of cross sectoral review powers. Further, according to the regulatory proposals, notifications to the Ministry are mandatory for all acquisitions exceeding the 25 percent, 50 percent or 75 percent mark.8 Accordingly, Germany is endeavouring to ensure more frequent and likewise more detailed reviews are performed for acquisitions in the fields of high technology and critical infrastructure. As a result, the general preparation process for successful transactions will be more laborious and is likely to include proposals to the investment control agencies.

In numerical terms, the number of review procedures is expected to increase. During the period from October 2013 to July 2017, a total of 383 acquisitions were reviewed, 36 within a formal procedure. Since the legislative reforms of July 2017, 62 acquisitions have already been reviewed, 39 within formal procedures. Compared to 2016, which had an overall number of 42 procedures and 2017 with 66, all signs point towards an increase to 100 procedures p.a.9 Once this stricter approach to foreign direct investments is fully implemented, in future emphasis for companies must lie on thorough foreign investment due diligence in M&A transactions.

3. Prospects for European FDI review rules

As far as upcoming developments on the EU plane are concerned, the plan is to develop a specific EU-wide mechanism, aiming at greater level of transparency and preventing negative effects on critical infrastructure, technologies and sensitive information. Currently, less than half of EU Member States have legislation in place that allows them to review FDI on grounds of national security or public order.10 The Commission proposed a draft legal text in September 2017, which some optimistically want to see enacted by the end of this year. The proposed rules primarily grant the Commission the authority to implement a security review of the investment and give a non-binding opinion to the relevant EU Member State in the case that EU interests are endangered. This complies with the EU‘s approach that “Foreign direct investments are a major source of innovation, growth and jobs [...] and keeping the EU open to investment is crucial, but the right tools to protect key technologies from strategic threats and ensure that our essential interests are not undermined are needed”.11

Future FDI Control in the U.K.

Similar endeavours have also been undertaken by the UK. The general aim behind proposed amendments is to screen investments, particularly of Chinese State-owned companies. Recently, the UK Government introduced legislation on national security regarding FDI in the sector of cutting edge technologies. According to this proposal, the Government can review transactions, where the turnover is expected to exceed £ 1 million, as compared to the current turnover threshold of £ 70 million. Reforms of the Enterprise Act 2002 will amend thresholds for review in the sectors of advanced technologies and dual-use goods. Here, the threshold for UK turnover is also lowered to £ 1 million and allows for the review of transactions with lower turnover rates where at least 25 percent of the relevant goods or services are supplied to the UK market.

Moreover, the Government Green Paper of 17 October 2017 on the Business, Energy and Industrial Strategy (BEIS) also contributes to developing a regulatory regime for screening and reviewing transactions, which raise national security concerns.

The guidance published on 15 March 2018 proposed two statutory instruments, respectively an affirmative statutory instrument and the negative statutory instrument for turnover thresholds. The proposed tests regard the development, design, and manufacture of and the supply of services for dual-use goods, computing hardware and in the area of quantum technology. Under section 23A of the Enterprise Act 2002, the military and dual-use sector includes enterprises involved in the development and production of goods specified in the relevant export control legislation.

In addition, since 2010, selected parliamentary committees have been allowed to take evidence from bidders and target companies in hearings. With the new rules adopted on 11 June 2018, the UK‘s merger control regime now places greater emphasis on regulating FDI, and introduces stricter threshold tests for businesses active in the military, dual-use, computing hardware and quantum technology sectors. According to these amendments, ministers can intervene where the UK turnover exceeds £ 1 million. This prospect points towards further, more comprehensive changes, with the prospect of a white paper which is expected to be published later this year.

FDI Control changes in the U.S.A.

As far as the U.S.A. are concerned, the latest development is Congress’ successful negotiation of the Foreign Investment Risk Review Modernization Act of 2018 (FIRRMA) adopted 13 August 2018.

With rules requiring a more comprehensive annual report, FIRRMA aims at increased transparency. For future inbound investments, the Committee on Foreign Investments in the United States (CFIUS, interagency body within the U.S. Treasury Department) undertakes a national security review. Further, the Act deals with jurisdiction, practices and overall administrative procedures of CFIUS in greater detail. As for the expanded and more detailed jurisdiction of the CFIUS, covered transactions can now be reviewed for a possible impairment of U.S. national security. If these negative effects are confirmed, the CFIUS is granted the authority to either amend or entirely block transactions. The protective scope of the FIRRMA includes critical technologies in the arms sector (subject to the International Traffic in Arms Regulations, ITAR or Export Administration Regulations, EAR). As for the administrative procedures, parties desiring FDI can now file for a short declaration clearing the transaction or apply for a full voluntary notice. With the rules under the FIRRMA, the CFIUS can define the U.S. substantial interests and submit transactions for review and further investigation. The new review timelines set out an extended timeframe of 45 days with potential extensions up to 60 days. In this regard, the annual report includes inter alia details on reviews with full notice, results of the cases and statistics on the length of the CFIUS review processes.

4. Conclusions

Although Germany still wishes to tighten its investment review policy, in light of the global trend towards greater security and essential public security goals, increases in the number of investment reviews will by no means knock Germany of the list of preferred business partners.

Nevertheless, investors should anticipate that more time will be devoted to preparation and constraints must be satisfied if an FDI is to be implemented successfully. Given the rapid increase in cyber criminality and the immanent risks that need to be faced in an increasingly complex globalised world economy, future FDIs should be designed true to the motto: better safe than sorry.

If you have any questions please feel free to contact Dr Rainer Bierwagen.

1.See generally the annual UNCTAD reports, here the latest “World Investment Report 2018” and more in detail “Chinese investment in Europe: record flows and growing imbalances”, joint report by MERICS andRhodium Group; January 2017; https://www.merics.org/en/china-flash/chinese-investment-europe- record-flows-and-growing-imbalances, and “EU-China FDI: Working towards reciprocity in investment relations”,by the same authors, April 2018, https://www.merics.org/en/papers-on-china/reciprocity.↩

2. See for an overview the Blog by Georg Philipp Cotta and Christoph Heinrich on the changes in 2017 at https://www.beiten-burkhardt.com/de/news/germany-tightens-its-rules-foreign-corporation-acquisitions-and-proposes-eu-regulation.↩

3. See the Blog by Georg Philipp Cotta and Christoph Heinrich at https://www.beiten-burkhardt.com/de/news/germany-tightens-its-rules-foreign-corporation-acquisitions-and-proposes-eu-regulation.↩

4. See the Blog by Georg Philipp Cotta and Christoph Heinrich on the Aixtron and LEDVANCE cases at https://www.beiten-burkhardt.com/de/news/aixtron-and-ledvance-climate-change-chinese-investments-germany.↩

5. Cf. https://www.verfassungsschutz.de/embed/vsbericht-2017.pdf pp. 279/280.↩

6. https://global.handelsblatt.com/opinion/germanys-china-syndrome-2-897518.↩

7. Among the most relevant investments are FDI in the Daimler AG, Kuka AG, Aixtron Se und 50Hertz Transmission GmbH, for more detailed view on Chinese investment preferences see: https://www.finanzmag.com/grossinvestor-china-setzt-auf-europa/.↩

8. https://www.politik-kommunikation.de/gesetz-des-monats/deutschlands-chinesische-mauer-2146963973; https://www.onpulson.de/33734/bundesregierung-will-chinesische-investoren-ausbremsen/.↩

9. http://www.manager-magazin.de/unternehmen/industrie/die-gruende-fuer-die-berliner-beschluesse-gegen-leifeld-und-50hertz-a-1221450-3.html.↩

10. http://www.europarl.europa.eu/legislative-train/theme-a-balanced-and-progressive-trade-policy-to-harness-globalisation/file-screening-of-foreign-direct-investment-in-strategic-sectors. ↩

11. Emil Karanikolov, Bulgarian minister for trade: cf.: http://www.consilium.europa.eu/de/press/press-releases/2018/06/13/screening-of-investments-council-agrees-its-negotiating-stance/.↩

Experts

|

Prof. Dr Rainer Bierwagen Rechtsanwalt Partner |

|